Pradhan Mantri Jeevan Jyoti Bima Yojana was launched by PM Sh. Narendra Modi Ji on 9th May, 2015. It is one of the 3 social security schemes launched by Government of India simultaneously. I covered Atal Pension Yojana in my previous post and next post will be dedicated to Pradhan Mantri Suraksha Bima Yojana. In layman terms, Pradhan Mantri Jeevan Jyoti Bima Yojana is a term insurance plan. It can be renewed annually. It offers life insurance cover for death due to any reason. As it is evident from my posts that i am a big fan of term insurance plans due to its inherent benefits. In my opinion, it is must for every Indian citizen. Currently, penetration of a Life Insurance is very low in India. Within life insurance, the penetration of a Term Insurance plan which is truly a Life Insurance cover is miniscule. Personally, i don’t consider Insurance cum investment plan like money back policy, ULIP etc as an Insurance plans. Low penetration of Insurance is due to lack of awareness or also due to the mindset that what we will be the returns on Investment.

Why Pradhan Mantri Jeevan Jyoti Bima Yojana is launched?

1. Increase Penetration of Life Insurance: As i mentioned that penetration of Life Insurance is very low at around 3% in India. Therefore, one of the reasons which i can think off is that Pradhan Mantri Jeevan Jyoti Bima Yojana is launched with an objective to increase life insurance penetration. Here penetration should not be considered quantitatively. There is a social message behind it. Assuming that something happens to an insured than the financials of the family goes haywire. Therefore, this term insurance cover will act as an immediate relief and provide financial security to the family of the insured.

2. Increase Awareness: By providing a basic cover of 2 lakh, Government of India would like to increase the awareness about the importance of Life Insurance (read Term Insurance). Once people will start realizing the benefits of an Insurance then they will definitely opt for personal cover to increase the insurance coverage depending on the requirement. Moreover, the USP of a scheme is Life Cover of 2 Lakh in less than Rs 1 per day. I think, this is the best way to spread the message and create awareness.

3. To activate accounts opened under Pradhan Mantri Jan Dhan Yojana: The biggest problem faced by the Govt of India is inoperative accounts under Pradhan Mantri Jan Dhan Yojana. Bank incur a certain cost to maintain the savings account, but inoperative accounts are basically a burden on the banking system. By introducing an auto debit facility for all 3 newly launched social security schemes, Govt will ensure that accounts will remain operative. By doing this govt, has hit 2 birds with a single stone

(a) Eliminated operational hassle to collect premium/installments of social security schemes

(b) Accounts opened under Pradhan Mantri Jan Dhan Yojana will remain operative

Snapshot of Pradhan Mantri Jeevan Jyoti Bima Yojana in 25 points

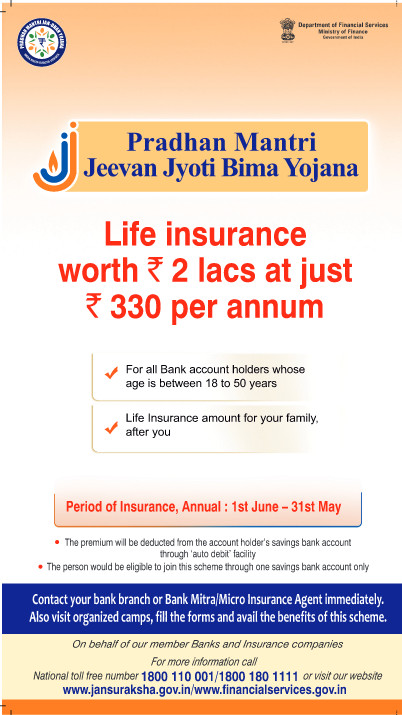

1. All Savings Bank Account holders are eligible for Pradhan Mantri Jeevan Jyoti Bima Yojana.

2. Min and Max Age of Entry is 18 years and 50 years respectively

3. An individual can avail only Single Plan under Pradhan Mantri Jeevan Jyoti Bima Yojana. In short, if he has 4 savings account then it doesn’t mean that he/she can opt for 4 term life insurance covers of 2 lakh each under Pradhan Mantri Jeevan Jyoti Bima Yojana.

4. Sum Insured under Pradhan Mantri Jeevan Jyoti Bima Yojana is Rs 2 lakh.

5. Life Insurance cover can also be availed by non-earning members like Housewives etc.

6. Annual Premium of Pradhan Mantri Jeevan Jyoti Bima Yojana policy is Rs 330. Premium is exempted from Service Tax.

7. The premium is subject to change in future and can be increased/decreased in future. Premium is fixed for first 3 years.

8. Insurance Cover will be applicable from 1st June to 31st May.

9. The subscriber can enroll for Pradhan Mantri Jeevan Jyoti Bima Yojana by giving an auto debit instruction before 31st May to avail the cover from 1st June. Late enrollment for prospective cover is allowed till 31st Aug or 30th Nov, 2015 as decided by the Govt of India.

10. All the future enrollments to this scheme will be on a prospective basis by paying FULL Annual Premium. For example, if you opt for this scheme on 1st Jan then your cover will be valid from 1st Jan to 31st May but you have to pay the premium for FULL Year.

11. You need to submit a certificate of Good Health which obviously everyone will declare that they are in a state of Good Health. Self Certification of Good Health is waived off during the initial enrollment period till 31st Aug, 2015 or 30th Nov, 2015 as decided by the Govt of India.

12. Insurance coverage is available only till the age of 55 years.

13. Insurance cover will lapse in case Savings account is closed by the account holder or due to low balance / insufficient funds in a bank account for the insurance premium.

14. If you avail multiple covers under this scheme knowingly or unknowingly then the premium of all additional covers will be forfeited except the single operative cover.

15. Break up of Annual Premium is as follows

Insurance Premium: Rs 289

Administrative Charges to participating Bank: Rs 11

Expense Reimbursement to BC/Corporate/Agent: Rs 30

16. Except Auto Debit facility, there is no other premium payment mode available.

17. During first 45 days from the date of start of policy, No Claim will be entertained except accidental death.

18. Some Banks like ICICI Bank have started enrollment for Pradhan Mantri Jeevan Jyoti Bima Yojana through SMS.

ICICI Bank customers can SMS PMJJY <nominee name> Y to 5676766 from their registered mobile number

19. The policy will not be issued if Nominee details are missing.

20. The insurance policy under Pradhan Mantri Jeevan Jyoti Bima Yojana is a Group Insurance policy, not an individual policy.

21. To download Subscriber Registration form in English, CLICK HERE

22. Official website of Pradhan Mantri Jeevan Jyoti Bima Yojana is http://www.jansuraksha.gov.in/

23. You can call on following toll-free no’s to get scheme details

National Toll-Free – 1800-180-1111 / 1800-110-001

To know helpline no of your state, Click Here

24. Consent of a subscriber for Auto Debit is required every year by the bank i.e. Auto Debit is not recurring in nature.

25. You can opt for any additional insurance cover/continue existing insurance cover along with cover under Pradhan Mantri Jeevan Jyoti Bima Yojana.

Suggestions

1. Option to opt for High Insurance Cover: I do agree that we cannot compare social security scheme from the personal finance perspective. The cover of 2 lakh is too low even for a middle class. Maybe in future, govt may provide an option to provide higher cover under Pradhan Mantri Jeevan Jyoti Bima Yojana at a higher premium. As the scheme is social security scheme therefore subscriber may top up the insurance coverage with personal term insurance cover.

2. Not too Cheap: Due to the base effect, Insurance premium appears to be too low but on a comparison with normal term insurance plan, it is not that cheap. I have insurance cover of 1.5 Cr for an annual premium of Rs 15000 excluding service tax. Which implies for 1 lakh coverage premium is 100 Rs. Therefore, for 2 lakh insurance coverage premium is 200 Rs. Obviously premium is low for high-value covers but at a macro level, premium under Pradhan Mantri Jeevan Jyoti Bima Yojana is almost at par with marked linked premium with an inbuilt discount of group insurance. As the coverage is not linked to age bracket therefore it is at par with a market rate for young people and discounted for people in 45 – 50 year age bracket.

3. Underwriting: This policy will be riskier for life insurance companies as no underwriting is being done. Ideally, insurance coverage and premium should have been linked to the age bracket of an individual. At the same time, product communication would have been difficult and complex in this scenario. I personally feel that at least there should have been the clause for Pre-Existing Disease as it would have helped to keep insurance premium in control. On the other hand, Pradhan Mantri Jeevan Jyoti Bima Yojana being a social security scheme, waiver of same can be justified.

You may post your queries/comments related to Pradhan Mantri Jeevan Jyoti Bima Yojana in the following comments section.

Copyright © Nitin Bhatia. All Rights Reserved.

Point no. 11 was not mentioned on ICICI bank..I have already subscribed in ICICI..

Self Certification of a Good Health is not required during initial enrollment period.

thanks bhatia sir

Thanks for the nice article. I agree that the premium is not competitive with other term insurance plan. However the plus point is that it covers non-earning members as well. I also understand that there is no exclusive policy issued for this insurance. The premium payment (auto debit) receipt should be submitted for claiming purpose. Please correct me if I’m wrong.

That’s correct.

Point 13. Will my insurance cover lapse if i change the bank, but still pay premium from other bank ?

Sorry i could not understand what you mean by changing the bank. If you close account then your insurance cover will lapse.

As Bala quoted, this term plan covers non-earning members…thats really good for non-working housewives